")

Written by Nick Ackerman, co-produced by Stanford Chemist.

XAI Octagon Floating Rate & Alternative Income Trust (NYSE:XFLT) continues to pump out a high yield for income-focused investors thanks to strong net investment income in a higher rate environment. The latest semi-annual looks to reaffirm the coverage remains strong with this fund. In fact, the latest report suggests the fund is on pace to deliver even higher NII over last year. With rate cuts being pushed back further and further, that also remains good news for this fund as that cash flow should continue to flow in.

XFLT Basics

- 1-Year Z-score: -0.99

- Premium: 2.02%

- Distribution Yield: 14.31%

- Expense Ratio: 3.88%

- Leverage: 38.89%

- Managed Assets: $678.7 million

- Structure: Perpetual

XFLT’s objective is to “seek attractive total return with an emphasis on income generation across multiple stages of the credit cycle.”

They will do this through “a dynamically managed portfolio of floating-rate credit instruments and other structured credit investments within the private markets. Under normal market conditions, the Trust will invest at least 80% of managed assets in senior secured loans, CLO debt and equity.”

The fund’s expense ratio is relatively high for a closed-end fund, but as we’ve touched on before, it’s actually low compared to the other collateralized loan obligation CEFs on the market.

This is helped by not being a pure-play CLO fund, but also notable is that they don’t have incentive fees like the other pure-play CLO funds. Those incentive fees are often earned whether the fund is earning positive returns or not, as they are based on the net investment income only.

When including the fund’s leverage expenses, the total expense ratio comes to 8.64%. The fund has seen its utilization of borrowings increase, with the latest semi-annual report now coming in at $169.05 million. That’s up from the $150.35 million they had outstanding at the end of fiscal 2023 and up from the $113.15 million borrowed at the end of fiscal 2022. As the fund grows in size due to at-the-market offerings and share offerings, they’ve continued to ratchet up the borrowings being employed by the fund to regularly maintain around a ~40% effective leverage ratio.

A portion of its leverage comes in the form of a preferred that is publicly traded, the XAI Octagon Floating Rate & Alternative Income Trust 6.5% Term Preferred (XFLT.PR.A). This comes with a current yield of 6.6%, which makes it a fairly sound choice for more conservative investors. I pair this up with my heavier position in XFLT to help balance it out. We’ve already crossed the call date of this preferred, as that occurred in March 2023. It does come with maturity of March 31, 2026, though, so it won’t be around forever.

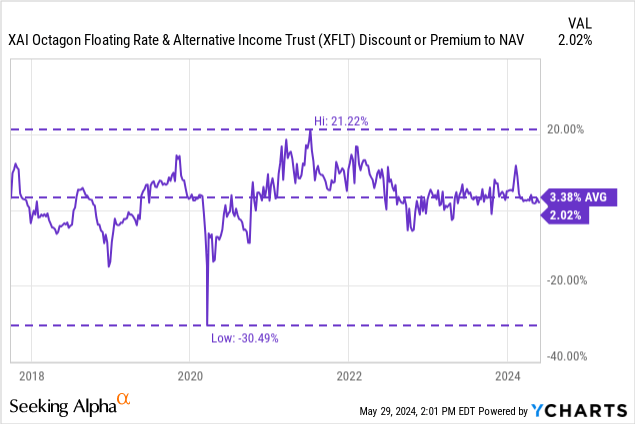

Performance – Premium Sticks Around

As we had noted previously, this fund has received approval for eliminating its term structure and changing to a perpetual fund. I had noted a few examples of that happening previously, where funds had subsequently fallen to discounts after going through such a change. It’s only been a relatively short period of time, but that has not been the case for this fund at this point. At least, nothing too material at this point. The fund’s premium was higher in our last update, but it remains at a premium.

The latest premium is consistent with its longer-term historical average and hasn’t gone to any extraordinary discount as we saw in a couple of the other cases.

YCharts

Of course, this continues to be a strong operating environment for this fund, with the higher rates still hanging around and the fact that rate cut expectations continue to get pushed back further. Higher rates bode well for this fund. Further, the fund benefits from an overall fairly resilient economy. This fund invests heavily in below-investment-grade companies and is leveraged.

So, any sort of economic downturn would likely see sharper drawdowns for this fund, making it a relatively riskier fund. In their commentary, they actually noted that the default rate had ticked lower on the Morningstar Leverage Loan Index. That’s good news.

But, there is the bad news as well. They noted that “distressed exchanges” had increased. That’s generally bad news, but it could also be better than the alternative of an outright default.

The trailing 12‐month default rate for the Morningstar LLI decreased to 1.14% as of March 31, 2024, from 1.34% as of September 30, 2023. 3 While conventional defaults (i.e., due to missed payments and bankruptcy filings) declined over the Period, the count of distressed exchanges increased. 3 Distressed exchanges occur when a debtor exchanges assets generally worth less than their original loan in an effort to restructure the debt. Distressed exchanges and other liability management transactions or “LMTs” (in which a company’s debts are restructured outside of a typical bankruptcy process), have become more prevalent between troubled companies and their lenders as a means to reduce debt and avoid costly bankruptcy proceedings. 3 We expect LMT activity to remain elevated in the near-term.

In the grand scheme of things, when you are looking at a 14% yield, you know you aren’t getting investments in triple-A issuers. As we’ve historically seen with a particularly sharp drop in Covid, it can be quite volatile. In my opinion, I believe investors are being fairly compensated in terms of risk/reward with XFLT.

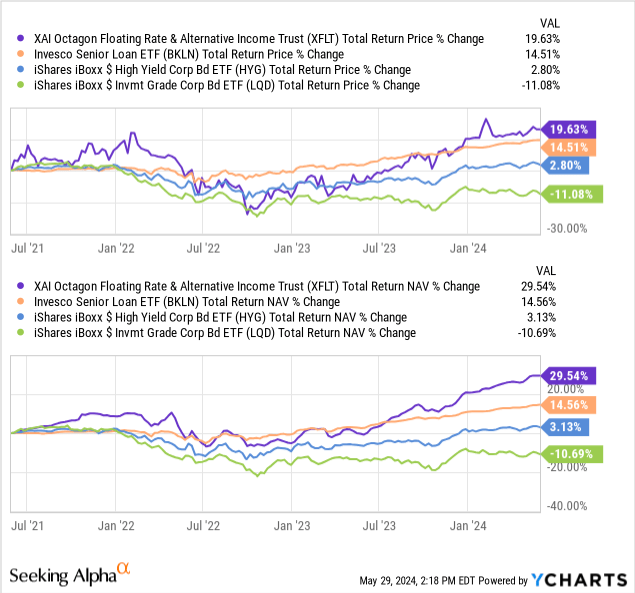

In terms of the performance of the fund, since its inception, the fund has beaten out its benchmark. In the last 1 year, the fund has completely stomped its benchmark total return by over double.

XFLT Annualized Performance (XA Investments)

Distribution – Solid Coverage Remains

With this latest semi-annual report, we are seeing the last six months of the period ending March 31, 2024, for this fund. Net investment income based on this latest figure would put NII coverage at nearly 102% for the current monthly distribution.

XFLT Financial Metrics (XA Investments)

In our previous update, we looked at the three-month quarterly financial report and noted the $0.27 NII per share figure. With that, it meant we saw a slight decrease in Q1 2024 NII as it would have delivered $0.25 NII per share. Overall, this is non-material and could easily be due to just timing with payments.

That means the fund’s strong 14.31% distribution rate continues to be achieved, at least through NII. After a rough drop in 2022, the fund also started to claw some of those losses back as well. That helped to contribute to the strong performance we saw over the last 1 year, where the fund saw its NAV rise while supporting such a high distribution, too.

It is important to remember, though, that as we look back at the last three years now—which include the Fed raising their target rate aggressively to stabilizing now since—XFLT has performed quite strongly on a relative basis. Higher interest rates saw significant pressure across the fixed-income space. Here is a look at ETFs that help represent other fixed-income areas. The closest peer to XFLT could be considered Invesco Senior Loan ETF (BKLN), as BKLN holds primarily floating rate-based securities as well.

We then have the fixed-rate debt ETFs that represent high yield and then investment grade corporate bonds, represented by iShares iBoxx $ High Yield Corporate Bond ETF (HYG) and iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD). An investor in HYG managed to barely break even over the last three years, while those in LQD are still looking at overall total return losses in this period.

YCharts

XFLT’s Portfolio

Since our last update, there hasn’t been too much to report on this front. They last reported turnover in their latest report at 19%, and that compares with 29% for the full 2023 fiscal year. That would put it on pace for a higher overall turnover rate than was reported in each of the prior three years.

While the managers certainly are changing positions around, as reflected in the fund’s turnover reported, the fund’s overall asset allocation has remained largely similar to when we gave it a look near the start of the year. That is, senior loans comprise the largest allocation of the fund. That remained quite similar to the previous allocation, which was 45.04%. That was followed up by CLO equity exposure as the second-largest then, followed by CLO debt, each of which previously represented allocations of 32.09% and 16.51%, respectively.

XFLT Asset Allocation (XA Investments)

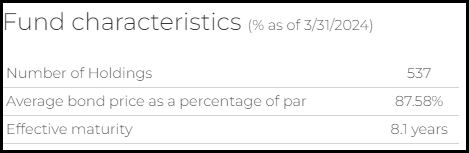

We’ve also seen the average bond price of the fund’s underlying portfolio climb slightly. This is fairly interesting to note because, essentially, as the fund’s premium itself came down, it was slightly offset by seeing a lower average discount in its underlying holding.

XFLT Fund Characteristics (XA Investments)

Finally, worth noting is the 537 number of holdings. One way that high-yield-focused funds protect themselves is through significant diversification. With risks spread across hundreds of companies, it limits the fund’s exposure and that just one or two individual failures will take the fund down substantially.

This is further reflected by the fund’s top ten holdings, with none representing an overly large allocation. Additionally, the CLO investments themselves contain hundreds or even thousands of loans pooled together. Of the largest positions listed here, most of them are CLO positions as well. To take down XFLT, we’d need to see a deterioration of the economy across the board.

XFLT Top Ten Positions (XA Investments)

Conclusion

I believe that XFLT remains an interesting choice for income investors who aren’t afraid to take a higher risk. In my opinion, the fund’s risk/reward is fairly attractive. They are covering the 14.4% yield that they are paying investors with the cash flow generated in the underlying portfolio. As long as rates aren’t cut, that should remain the case as well.

However, being highly leveraged and investing primarily in below-investment-grade securities means there is always the potential for a black swan event to swiftly see a 50% drop in the fund. At the end of the day, you aren’t getting this type of yield because you are gaining exposure to pristine triple-A-rated debt instruments.

The premium has come down slightly since our prior update. Our target ‘Buy’ discount/premium is actually parity, or, in other words, any discount on this fund would be what we are looking for to add to this position. While the premium remains nearly at this target, I’m quite comfortable adding at these levels and wouldn’t be too picky.

Read the full article here

")

")

")

")

")