")

Investment Thesis

Company Overview

LendingTree (NASDAQ:TREE), incorporated in 1996 and headquarters in Charlotte, North Carolina, is a platform that connects borrowers and lenders by matching based on the private information borrowers provide under various brands such as its namesake website LendingTree. The company has three reportable segments: Home, Consumer and Insurance.

Strengths and Weaknesses

As the news flashed, on or around June 10 LendingTree was breached by hackers. The company uses Snowflake (SNOW) for its business operations and was notified by the company that its QuoteWizard subsidiary may have been affected. Subsequently, the leak was confirmed, and the hackers auctioned off the leaked customer data on cybercriminal forums online. Morgan & Morgan is investigating the case regarding LendingTree’s practice with respect to the borrowers’ data.

There is a saying, if you are not paying, then you are not the consumer but the product. It works very well in the case of LendingTree. As the company disclosed in the 10K, its Network Partners pay the upfront match fees to receive customer requests, and/or upfront fees for clicks or call transfers, which are the source of its revenue. That means, LendingTree is essentially the dealer of the borrowers’ information to lenders in its network. Therefore, we won’t refer to the borrowers as customers of LendingTree because its customers are actually the lenders. This makes its data breach a much closer hit to its bottom line than it is made out to be.

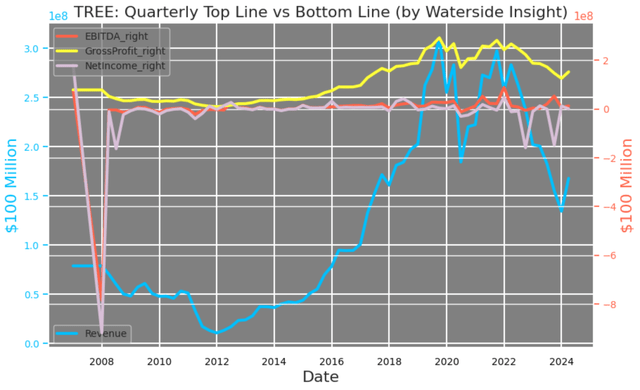

LendingTree: Quarterly Top Line vs Bottom Line (Calculated and charted by Waterside Insight with data from company)

Dissecting its revenue decline by segment shows Home lending declined the fastest, which went down another 30% YoY in the quarter ending in March. Its Consumer segment fluctuated in the past four years, and now is back to where it was in 2021 Q1. It used to report Credit Cards as part of the Consumer segment in 2022, but that has been taken out or perhaps merged with the “Other Consumer” subsegment, likely due to a shrinking revenue size. The only segment that holds steady is Insurance, which has been at or around $80 million per quarter, while other segments were declining during the same time. Looking back on the company’s history, it actually started its business in the home lending business, such as matching borrowers with mortgage lenders, in the 1990s. This should be the space in which it has the most expertise and network strength. To see its Home segment falling in such a fashion twenty-plus years later raises the question of what its core strength really is.

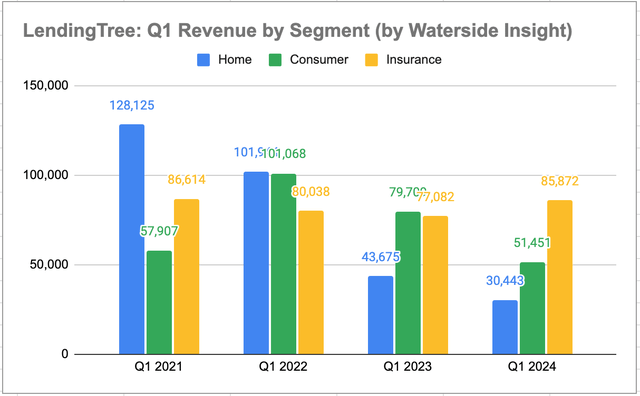

LendingTree: Q1 Revenue by Segment (Calculated and charted by Waterside Insight with data from company)

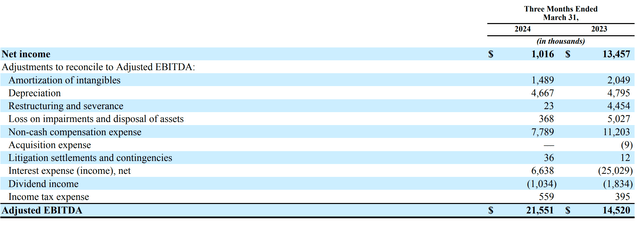

Margin-wise, it has maintained most of them surprisingly smoothly except for the Net Margin even with its revenue going through large changes. Its EBITDA margin in particular is recovering quickly from the low in last year. But its net margin has fallen to negative 20%, which it hasn’t been for the past ten years. The reason for a lower net income leading to a higher EBITDA was mostly due to interest expenses, as its 10Q shows.

LendingTree: Q1 2024 vs 2023 EBITDA Comparison (Company 2024 Q1 10Q)

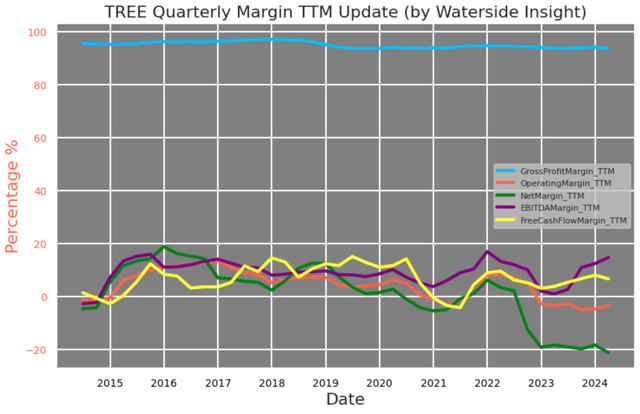

LendingTree has a very small cost of goods, about 6% of its revenue. As we discussed earlier, the product it is dealing is essentially borrowers’ information and borrowing requests. Its main function is to sell this information to a massive network of lenders. So the major overhang to its net income and earnings is the operating expenses. It produces a gross margin of 91.24% but only a 0.6% net margin after taking out the operating expenses. Among the different expenses, the selling and marketing expenses account for approximately 76% of the total operating expenses in the last quarter. In its 10K, LendingTree talked about the importance of brand recognition in attracting and retaining customers. Relating this back to what we inferred from the decline of its Home segment earlier, the brand recognition didn’t seem to have built up in all areas of its business. The more its revenue weakens, the harder it spends on sales and marketing offers another clue into its core strength. This explains why its net margin declines the fastest when its revenue comes down from the peak.

LendingTree: TTM Quarterly Margins (Calculated and charted by Waterside Insight with data from company)

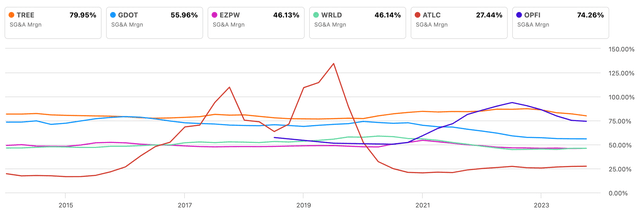

Even among its peers, it has the highest SG&A margin, which is the sales, general, and administrative expenses as a percentage of revenue. As a company established in the 1990s, its brand recognition doesn’t seem to endure over time.

LendingTree: Peer Comparison of SG&A Margin (Seeking Alpha Stock Analysis)

Now back to the data leak. In LendingTree’s 10K, the company has listed various risk factors. Not the least, there is one regarding personal information as the following:

Our collection, use, storage, disclosure, transfer and other processing of personal information could give rise to significant costs and liabilities, including as a result of governmental regulation, conflicting legal requirements or differing views of personal privacy rights, which may have a material and adverse impact on our business, financial condition and results of operations.

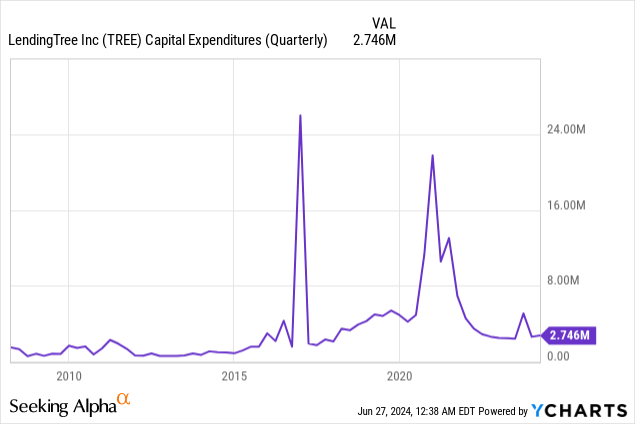

LendingTree does purchase cyber risk insurance to cover the claims in the aftermath of such incidents. But to safeguard its essential product, which is the borrowers’ information, LendingTree needs a robust risk mitigation infrastructure. In its 10K and recent 10Q, LendingTree explained that the CapEx spending was mostly used for internally developed software. It does have a Chief Information Security Officer (“CISO”), who is responsible for “the assessment and management of cybersecurity risk” and reports to the CEO and the Audit Committee. Its CISO gave the following words regarding the incident:

This is an ongoing investigation, and as soon as that investigation is complete, we will notify all the impacted customers.

There hasn’t been any official release on its website about it. Given its CapEx spending of $2.75 million on a quarterly basis for the past year or so, which also has to cover internal software development, the budget for cybersecurity risk mitigation is perhaps at a minuscule level or about 1% of its ballooning operating expenses as a comparison, even if it is completely outsourced to Snowflake. This creates an ongoing cybersecurity risk vulnerability for LendingTree, meaning the recent hacking incident could happen again if nothing is changed.

What we see from LendingTree’s financials is a struggle to increase its declining revenue without significant sales expenditure, while only minimally investing in the protection of its core product. Part of marketing spending has to do with its relatively weak brand recognition compared to its long history in the business. Data leak incidents will only further burden its branding, which could lead to more sales spending and weaker margins going forward. It’s a cycle that LendingTree needs to prevent proactively.

Financial Overview & Valuation

LendingTree: Financial Overview (Calculated and charted by Waterside Insight with data from company)

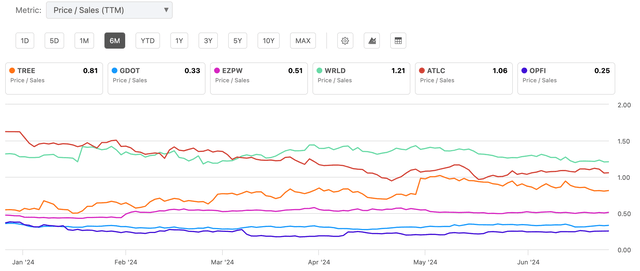

LendingTree lands in the middle range of the lowest Price-to-Sales ratio among its peers, according to Seeking Alpha’s analytics. We picked this ratio because its near-term challenge of boosting sales in order to recover its margins. But most of these alternative financial service firms have their own lending practice, while LendingTree has only one standout core function, which is product sales. Its sales should be strong with respect to price. This makes even its mid-range ratio look high.

LendingTree: Price to Sales Ratio (Seeking Alpha Stock Analysis)

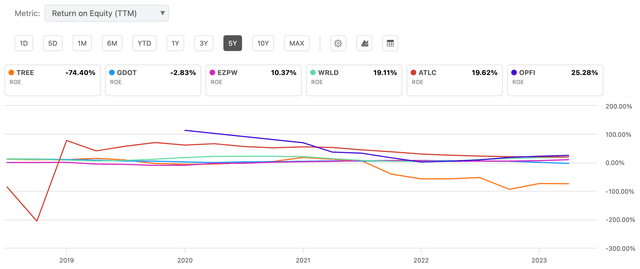

But its return on equity in a five-year period is at the lowest. Based on the risks we discussed above, it is possible that if its net margin does not recover, it could lead to other margins to deteriorate. The return prospect may not improve quickly. From this perspective, the stock is overvalued, even if it is not expensive among its peers.

LendingTree : Return on Equity Peer Comparison (Seeking Alpha Stock Analysis)

Conclusion

The recent data breach at LendingTree has caused damage to the borrowers that use its platform which could result in claims, but most importantly, it is a blow to its brand recognition and its core product strength. From a broader perspective, even without the data leak, the company is in a weak position in terms of its sales and margins. We think there are more vulnerabilities ahead, given how costly it is for it to acquire and retain borrowers, while on the other hand, cybersecurity could still be a risk going forward. We recommend a sell at its current price.

Read the full article here

")

")

")

")

(NYSE:KMI)")