")

Ingles Markets (NASDAQ:IMKTA) has reported two quarters of financials after my prior article on the company. Ingles Markets has started to report a tiny year-over-year decline in revenues along with weaker profitability as margins retract back to a more normalized level.

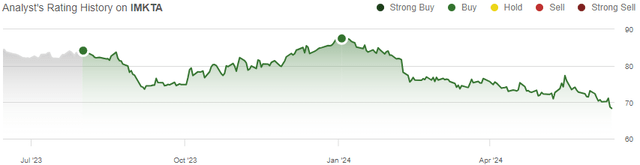

In my previous article, titled “Ingles Markets: Still Low-Risk And Cheap”, I rated Ingles Markets a Buy due to the company’s low valuation relative to its risk profile. The follow-up article was published on the 3rd of January in 2024, after I initially rated the stock a Buy in August of 2023. The stock has since lost 22% of its value compared to an S&P 500 return of 15% from the publishing of the previous article, as results have lowered back closer to historical averages in recent quarters.

My Rating History on IMKTA (Seeking Alpha)

Ingles Markets Showed Revenue Weakness in H1

After a long-term history of modest growth in line with inflation, Ingles Markets has reported revenue declines in FY2024 so far with -0.8% in Q1 and -1.0% in Q2. Food inflation has slowed down, and other companies such as BJ’s Wholesale Club (BJ) have even related to temporary food deflation in the beginning of 2024. The United States’ Bureau of Labor Statistics has shown estimated year-over-year inflation of 1.0% to 1.2% in the “food at home” -category in early 2024 so far, showing deceleration from pandemic-time highs.

Gas prices have also pushed growth into a weaker level, as retail gas prices show deflation during Ingles Markets’ Q1 and Q2. With these factors in mind, I don’t believe that the weak revenues are a sign of any underlying company-specific weakness, but rather temporarily slower industry growth as inflation fluctuates. Weakness seems to be continuing into upcoming quarters, but should subside into more stable historical growth in coming years – the recently weak stock performance seems to be unjustified fear from the markets.

Margins have weakened back into a more historical level as sales growth has halted – currently, the operating margin trails at 4.0%, down from the FY2021 high of 6.8% but still higher than the average of 3.3% from FY2014 to FY2019 prior to the pandemic and high inflation. With the recently higher capital expenditures partly related to technology investments and a milk processing plant, the operating margin will likely eventually land near the pre-pandemic average in my opinion, with some potential to stabilize slightly higher.

Balance Sheet Has Underlying Value

An aspect that I haven’t previously touched on is Ingles Markets’ valuable assets – the company has built the grocery store network, and owned $1128.7 million in buildings and $345.6 million of land after FY2023 based on their book value on the balance sheet. The realizable value of potential land sales is unknown, but should represent an incredibly significant amount especially when considering Ingles Markets’ current market cap of around $1.3 billion.

A potential sale-and-leaseback of the owned assets could create a lot of shareholder value – the cash proceeds would likely cover a significant amount of the entire market cap, and assuming a sale value at the book value and a rent yield of 6%, the paid annual leases of $88.5 million would only cover for 38% of current trailing operating income leaving space for healthy earnings.

Another potential way for the assets to create value would be a larger operator’s acquisition of Ingles Markets – the assets should be able to attract quite good potential acquisition offers for a larger grocery chain to optimize the capital structure.

The company’s founding family still owns a controlling share of the company, potentially limiting asset sales or M&A transactions due to quite a conservative historical approach. In light of quite limited strategic moves in the past, I don’t expect Ingles Markets’ underlying value to be likely to be realized to shareholders at least in the near future.

Ingles Markets’ Stock Undervaluation Remains

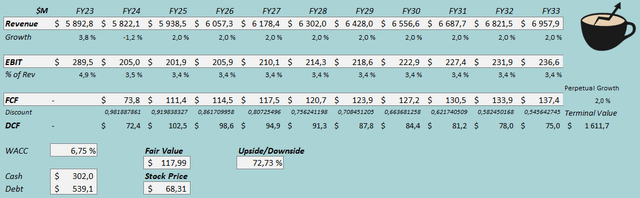

I updated my discounted cash flow [DCF] model from my previous estimates – I now estimate weak revenue growth in FY2024 of -1.2% compared to 1.0% previously. Afterwards, I still estimate stabilized growth of 2%.

Since the profitability has weakened faster than I anticipated previously, I have adjusted my long-term EBIT margin estimate accordingly. Previously I estimated a stable EBIT margin of 4.0% as inflation stabilizes, but I now adjusted the margin lower into 3.4% closer to the pre-pandemic average.

DCF Model (Author’s Calculation)

The estimates put Ingles Markets’ fair value estimate at $117.99, 73% above the stock price at the time of writing -the stock continues to be undervalued at a current trailing P/E of 7.4, very atypically low for a low-risk grocery chain. The fair value estimate is down from $136.47 previously due to lower margin estimates, but the DCF model still continues to expect very good upside.

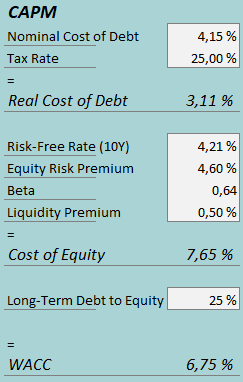

A weighted average cost of capital of 6.75% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q2 Ingles Markets had $5.6 million in interest expenses, making the company’s interest rate 4.15% with the current amount of interest-bearing debt. I keep my debt-to-equity ratio estimate the same at 25%. To estimate the cost of equity, I use the United States’ 10-year bond yield of 4.21% as the risk-free rate. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. I continue to use the previous beta estimate of 0.64. Finally, I add a liquidity premium of 0.5%, creating a cost of equity of 7.65% and a WACC of 6.75%. The WACC is down 7.25% previously.

Takeaway

Ingles Markets’ revenue growth has halted into slight decreases as food inflation has slowed and as gas prices show weakness. As a result, the company’s margins have fallen closer to the long-term pre-pandemic average, which I now estimate to be the baseline profitability going forward. The stock continues to be undervalued by the market as Ingles Markets provides healthy and low-risk cash flows. With strong real estate assets on the company’s balance sheet bringing underlying value, and as the stock continues to be undervalued by a good margin, I remain with a Buy rating for Ingles Markets.

Read the full article here

")

")

")

")

")