")

")

Early this year I issued an article on British American Tobacco (NYSE:BTI) arguing that the multiple is so low that it provides an inherent safety in terms of keeping the downside risk limited. Plus, the argument was that so depressed multiple warrants a very enticing entry point for investors to capture high yielding dividend streams. In addition, looking at the underlying business profile it was clear that the business is at a much safer position than what could be implied by the multiple (i.e., P/FCF of 5.1x).

As a result, the recommendation was to go long BTI, considering it an enticing dividend play with greater odds to capture incremental upside than experience a decline in the share price.

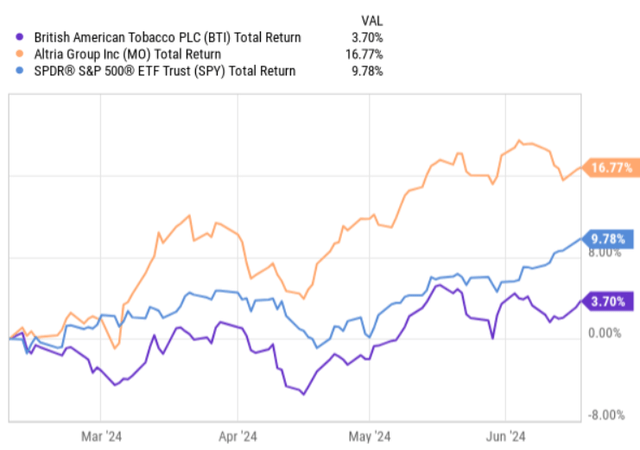

Since the moment when my bull thesis was published, BTI has delivered positive total returns, but underperformed its closest peer Altria Group, Inc. (NYSE:MO) as well as the S&P 500.

Ycharts

There are multiple reasons behind this divergence of returns. For example, the case with Altria is quite specific, where the company really managed to exceed the expectations by issuing a very strong Q1, 2024 report. More details could be found in my article on Altria here.

However, the key reason why BTI has stayed range bound and not followed the path of Altria and Philip Morris International Inc. (NYSE:PM), which has also registered double digit total returns over the comparable time period is mostly related to the new data points stemming from the First Half Pre-Close deck.

With this in mind, let’s now assess these new data points and see whether the bull case still remains intact.

Thesis review

If we look at the recent data points on a high level, we will quickly understand why the market has kept the BTI’s share price flat, while for MO and PM the market cap levels have surged higher.

The key reason lies in a combination of a negative growth that is expected to take place over the H1 period and some general headwinds that are mostly associated with the strengthening of a higher for longer scenario.

BTI’s financial performance is expected to be somewhat negative in the first half of the year (for which the earnings are still not out) due to front-end loaded wholesale inventory movements related to continued investment in BTI’s U.S. commercial segments as well as a phasing of new launches.

On top of this, H1 volumes and total revenues are expected to be negatively impacted by a stronger comparator relating to the price repositions in Japan and Italy (including also some phased rollouts of BTI’s new innovations this year).

Speaking of negatives there are also pressures stemming from more challenging U.S. macroeconomic backdrop, where the bulk of consumers continue to experience consequences and limited spending capacity from the higher interest rate environment.

Finally, it is clear that the battle with illicit flavoured single-use vapours is not bearing the necessary fruit, where the combustibles industry volume has dropped by around 9% on a YTD basis.

Considering these aforementioned dynamics, I think it would be fair to say that there is at least partially justified basis for BTI’s stock price remaining flat.

However, here is the thing.

While BTI has confirmed that H1 sales and adjusted profit from operations will decrease by low-single-digits, the projected positives in H2 should at the end of the 2024 offset the H1 challenges, rendering the full year positive in terms of revenues and profits.

There are several drivers behind this, but the key one is that the lion’s share of the pre-announced investments (mostly via organic growth avenues) will be completed by the end of H1, which, in turn, implies that only in H2 there will be a direct positive hit to top-line and (mostly) profitability levels.

Plus, there are two additional tailwinds for H2 results, which should help BTI achieve positive overall results for 2024:

- The number of trade representatives has now increased by 10%, which will help further expanding BTI’s retail contract coverage.

- This month BTI has started to roll out its new single-use vapour, Vuse Go 2.0 with more significant launchers planned through the remainder of 2024. This should clearly help drive volume and revenue performance in the second half.

Moreover, in the First Half Pre-Close Trading Update Conference Tadeu Marroco – Chief Executive – gave a nice color on how he sees the macroeconomic environment shaping out:

Looking at the broader macro context, we see some early positive macro indicators with real wage growth and strengthened aggregate household balance sheets. In addition, consumer confidence has started to track more positively since the end of last year. While the recovery is slower than we had expected at our results in February, we continue to expect some improvement in macros as we move through the second half, which is expected now to benefit our 2025 delivery.

So, putting these things together, BTI still expects the 2024 results to land at a positive sales and adjusted profit growth level.

Finally, if we couple this with the favorable dynamics at the capital structure level, I see no reason why the bull case should be changed. In terms of the capital structure dynamics, BTI has so far this year partially monetized its stake in ITC, which will enable a more accelerated share buyback program (~ GBP 700 million in 2024 and ~ GBP 900 million in 2025). In this context, we should appreciate the fact that relatively recently the S&P revised their outlook from negative to stable due to a sound deleveraging progress in conjunction with a narrowed leverage corridor. Also, in March this year, Fitch upgraded BTI’s rating to BBB+ stable outlook.

The bottom line

The double digit delta in YTD total returns between BTI and its closest peers Altria and Philip Morris is only partially justified. It actually creates an opportunity for investors to enter before BTI’s share price convergences closer to the peer levels.

The key reason why BTI’s share price has not jumped higher together with the peers is related to the deteriorated H1 performance. Yet, the underlying drivers behind the likely negative sales and adjusted profit levels in H1 are of a temporary nature. Most importantly, considering the fact that many H1 investment initiatives will come online only in H2, inventory movements are set to balance out after H1, and that the new rollouts of Vuse Go 2.0 will be facilitated more actively through the remainder of 2024, the results in the second half of the year will likely lead to a positive organic growth for the 2024.

In the meantime, BTI has accessed additional liquidity through partial ITC monetization and strengthened its capital structure that has also been recognized by two credit rating agencies.

In a nutshell, British American Tobacco at a P/FCF multiple of 5.2x, which is much lower than at what Altria and Philip Morris trades (8.8x and 17.6x, respectively), and given the positive growth prospects is a huge bargain.

As a result, in my opinion, British American Tobacco is still a buy.

Read the full article here

")

")

")

(NYSE:KMI)")

")

: A Strong Loan Book, But Earnings Are Under Pressure")