")

My thesis

Alibaba (NYSE:BABA) is a massively undervalued stock, according to my intrinsic value calculations. Nothing is that cheap with no significant risks, and investing in BABA is apparently extremely risky. The “Cold War” between the United States of America and China is a strong factor weighing on stock prices of Chinese companies. However, it is important to keep in mind that any war, whether hot or cold, ends in peace. Even the Cuban Missile Crisis, when the U.S. and USSR were not far away from starting a nuclear war, ended up in peace. There are numerous fundamental reasons why Alibaba is a good investment, especially at its current unrealistically low valuation. The stock is a solid high-risk and high-reward investment, deserving a Strong Buy rating at this share price.

BABA stock analysis

Sometimes Alibaba is called “Amazon of China” because both companies’ flagship businesses are the e-commerce and cloud. While Alibaba is mostly local cloud player, and is miles behind Amazon (AMZN) in terms of the global market share, there are some ways in which Alibaba is stronger. For example, according to statista.com, the cumulative gross merchandise value (GMV) of Taobao and Tmall is higher than a trillion USD and is almost 30% larger than Amazon’s GMV. Both Taobao and Tmall are owned by Alibaba.

statista.com

Apart from commanding the number one spot as the world’s largest e-commerce company by GMV, several Alibaba’s profitability ratios are higher compared to Amazon. The fact that Alibaba’s per employee revenue and net income are two times higher suggests that the business is very efficient.

Seeking Alpha

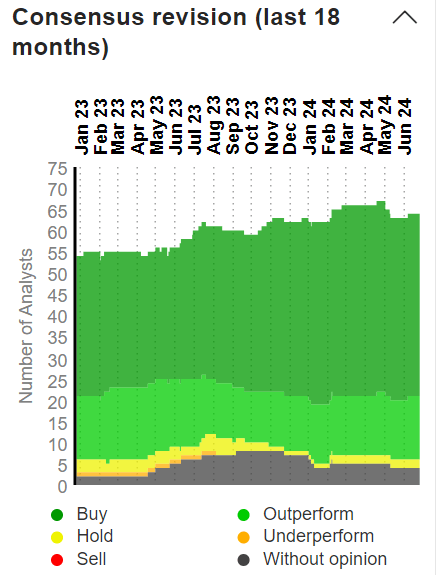

Please do not misunderstand me, I do not want to say that Alibaba is a better investment than Amazon. To make such a conclusion, I have to deep dive into Amazon’s fundamentals as well, and it is not a purpose of my BABA thesis. What I want to emphasize with these comparisons is that Alibaba’s crucial business metrics are competitive with Amazon. I am highlighting this factor because Amazon consistently mostly has Buy ratings from Wall Street analysts, shown in the below picture.

marketscreener.com

Amazon’s dominance in the global cloud market via its AWS business is undisputed, and it is far ahead of Alibaba in terms of the global market share. However, Alibaba is leading in its domestic cloud market, well ahead of Tencent (OTCPK:TCEHY). Being the number one local Chinese cloud company is also a big achievement and puts BABA into the pole position in the Chinese AI industry, especially taking into account a forecast that China’s AI industry will represent 30% of the global market by 2035. The forecast might be too optimistic considering the source named China Daily. However, I think that the AI industry in the world’s second economy by default has bright prospects.

China’s gross manufacturing production represents 35% of the world’s output, which makes it the world’s undisputed leader. AI in manufacturing is likely to be a hot trend over the next decade, with Grand View Research projecting a 44.2% CAGR by 2030. Alibaba’s dominance in the Chinese cloud industry and the country’s massive manufacturing production volumes makes the company firmly positioned to capitalize on the hot “AI in manufacturing” trend.

Now I want to explain why geopolitical risks are highly likely to be significantly overestimated by the market. The Cuban Missile Crisis between the U.S. and Soviet Union took place in 1962, more than 20 years before the term “Globalization” was invented. It was late the 1970s and early 1980s when global trade started growing exponentially. According to the below chart, in 2022 the global international export was worth around $25 trillion. It is 192 times higher compared to 1960, the year close to the Cuban Missile Crisis.

statista.com

What I want to say here is that the original “Cold War” between the USSR and USA ended up in peace, even when there was no globalization and countries were much less involved in international trade. I do not have data about the total value of imports and exports between the U.S. and USSR in 1962, but it is quite unlikelier than it was higher than the value of total trade between the U.S. and Russia in 2021 with only $36 billion out of America’s total $4.7 trillion in cumulative exports and imports.

Wikipedia

Economic ties between the U.S. and China are much closer, as China is the third-largest trade partner after the two closest neighbors. It is widely known that most of the America’s largest corporations have their manufacturing facilities our outsourcing partners in China, with almost 95% of Apple’s (AAPL) products are produced in this country.

Therefore, it is almost certain to me that the end of the current tensions between the world’s two largest economies is just a matter of foreseeable future. To conclude this part, I think that the market significantly overestimates Alibaba’s geopolitical risks.

Intrinsic value calculation

Discounted cash flow (DCF) valuation approach is the one I use to determine the intrinsic value of Alibaba. The approach’s name suggests that I have to figure out the discount rate, or WACC for Alibaba. In the below working, I outline how I arrived at a 6.3% discount rate for BABA’s DCF model.

DT Invest

Revenue forecasts from Wall Street analysts are quite conservative for Alibaba, projecting mostly single-digit revenue growth rates by FY 2034. Conservativeness is crucial for a DCF model, making me use these Wall Street estimates. Levered FCF margin on a TTM basis is 13.04%, which is lower than the last five years’ average. Therefore, I do not incorporate any metric expansion in the future. The perpetual growth rate is also very conservative at 2%.

In my second working below, all the described assumptions are incorporated into the DCF model, and it says that the company’s intrinsic value is $676.4 billion, almost four times higher than BABA’s market capitalization. Thus, the valuation is extremely attractive.

DT Invest

What can go wrong with my thesis?

From my BABA stock analysis and intrinsic value calculation, it might look like investing in this company is like a no-brainer. But in fact, it is not, and there are certainly some risks.

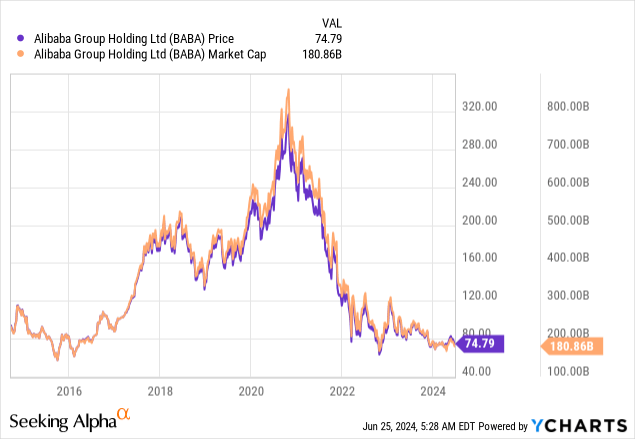

Despite all the theoretical advantages of buying the stock, the potential upside might remain “potential” for quite long. The stock price chart might make some investors pessimistic because the stock is now cheaper than its IPO levels, and it was a long time since the last big rally in BABA. Apart from geopolitical tensions, there are also political risks for the company within China. Actually, political risks were the first ones to trigger BABA’s rapid fall from its all-time high of October 2020 when Jack Ma suddenly disappeared.

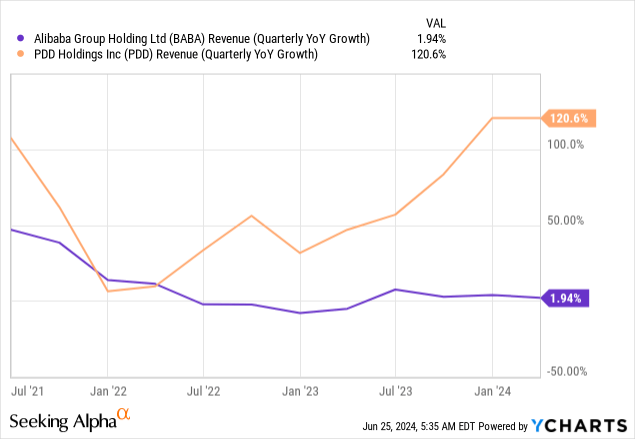

If we ignore these apparent geopolitical headwinds, there are more business-specific risks for Alibaba. For example, it has strong competitors, especially in ecommerce. There is a company called PDD Holdings, which demonstrates rapid revenue growth, while Alibaba’s revenue is almost flat. Of course, it is easier to drive PDD revenue growth against its current TTM $41 billion revenue compared to Alibaba’s $130 billion over the same period. However, this trend should not be ignored as a risk factor for BABA.

Unfortunately, Alibaba is not a stock that frequently delivers big earnings surprises, and its EPS revisions were quite disappointing in recent quarters as well. For many companies like Nvidia (NVDA) delivering positive earnings surprises works as a strong catalyst for stock price rallies. However, based on Alibaba’s recent surprises history, this catalyst is unavailable for BABA investors.

Seeking Alpha

Summary

I think that the potential upside for this giant conglomerate is too attractive to ignore, especially considering Alibaba’s dominance in the global ecommerce industry and its strong potential to become the undisputed leader in the thriving Chinese AI industry.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

")